Quick question, I don't work in the HFT field (I trade only options for fun on the side) but would anyone in the field care to comment whether a startup fund say, with a back-tested strategy would still be able to compete with the likes of HFT firms, provided that they have (1) sufficient capital, >$500K, (2) sponsored access/co-location to markets by proxy, e.g., Lightspeed, Lime Brokerage that provides the lower fee-structure plus the rented rack-space on the exchange data-centers, (3) historical and realtime quote feeds for forward and back-testing.

I imagine HFT entities who are broker-dealer agencies have even lowered fee structure; but it sounds like simple market-making on equities is no longer an easy business to be in due to the lowered spreads and crowded competitors.

So I'm wondering if a startup funds with the rented access could compete with the big boys in the options, futures, other derivatives and even bonds space where the latency still haven't caught with the equity market yet.

HFT represents a spectrum of strategies when described in the news. For the most part, I would argue you are describing a "quant trading shop" and would avoid the HFT label since it doesn't apply (HFT really means that you're gaming Reg NMS).

The type of shop you're describing might be able to compete, assuming you've identified a niche product with a margin that will still exist in 6 months. Backtesting is useful, but it is so bloody hard to accurately incorporate liquidity that I place little value on simulated results when it comes to short duration trades. You really have to jump in and test live, which represents the largest barrier to entry: established shops have the infrastructure & capital to try new ideas. When I was trading, we tested half a dozen new ideas every month in addition to "production trades".

High frequency, IMO, should really be used to identify hardware intensive strategies co-located at the exchanges and utilizing telecommunications strategies not readily available to the market. For example, FPGA and dedicated microwave towers.

Lime is excellent, btw, but you really need some volume to justify them. For options at your level of capital, Interactive Brokers and long gamma trades look more attractive to me. Many would disagree and people do starve waiting for long gamma, but my memory is biased after seeing the little group next to me lose $40m in a week on a stupid short gamma "sure thing" based on back tests and other such nonsense. Oh, what a fun time that was.

Reg NMS requires that brokers fulfill orders at the lowest possible rate first. So if an HFT shop sets a trap for you on one exchange (offering 100 stocks a tiny bit cheaper), your broker would have to trade in that first. The HFT would then front-run you to the other exchanges, buy up what it can, and sell it back to you a bit higher. They can do this because they have lower latency. Add dark pools to the mix and the opportunities become even bigger.

This has been pretty thoroughly debunked. I don't really think this ever happened. There is just way too much uncertainty and risk to ever get an edge.

Remember HFT worship at the alter of the law of large numbers, meaning they get a 51% edge and ratchet up the frequency. So a typical strategy might be 48% profitable, 40% wash and 12% unprofitable.

0+ orders on the other hand, now that was a profitable strategy while it lasted:)

Would avidly read the comment adding some detail to this. :)

The book you link to in that comment (_Flash Boys: Not So Fast_) is really fantastic. It strikes me as being written in a style especially congenial to nerd message board people like me: detailed, episodic, point-by-point takedown. It's like a very long Reddit comment, and I mean that in the best way.

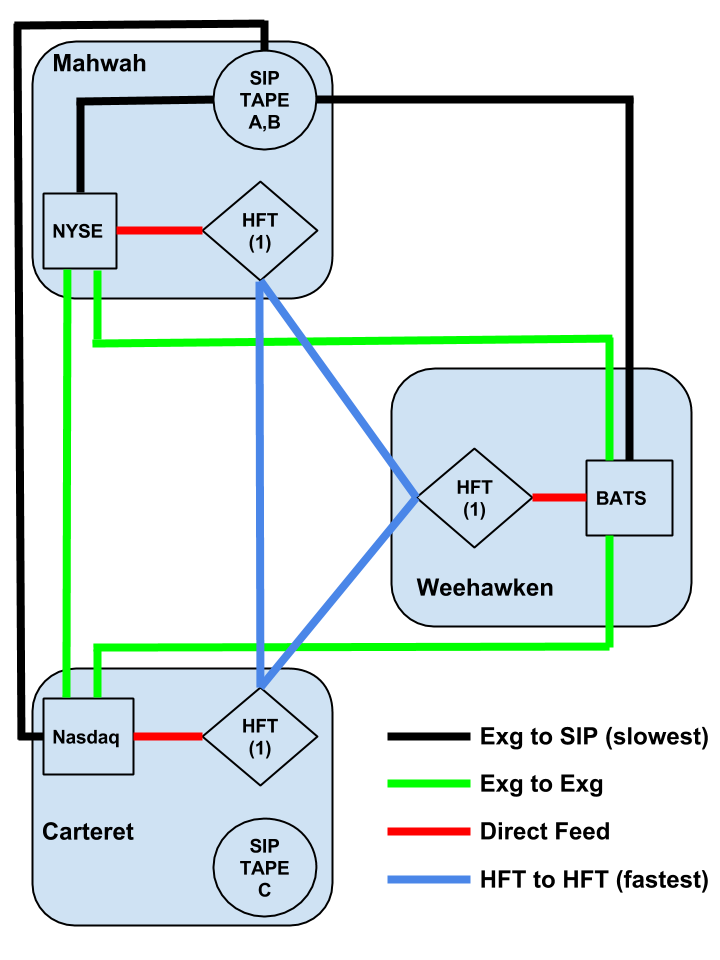

Long story short. RegNMS said people have to get the best price for their order. Now in a distributed system, which the US fragmented markets are, you know you can't know for cetain what hte state of the world is.

warning simplification ahead

Each market and dark pool has to trade at the price currently listed by the SIP. Now the sip is old and slow. Exchanges offer 2 prices sources,

- the SIP as legally requried

- a direct feed, which serious traders use.

The direct feed is faster, so by the time an exchange (A) reports a trade to another exchange(B) via the sip, the HFT guys who own their own microwave radio lines have notified their computers at exchange B, and moved their orders.

I was curious about microwave radio lines so I did a little digging[1]. It appears that microwave radio can double the speeds of fiber. Though the towers are limited by distance (max ~60mi separation), HFT shops buy/rent microwave tower networks connecting cities. For example, one HFT firm owns a network of ~30 microwave towers connecting NJ to IL that transmit 1.6 ms faster than fiber.

I see your point about the risk, but is there really that much activity in most stocks that getting to the top of the sell pile would be a large enough issue? As I understand some order types were more or less designed to give HFT an edge.

Although I suppose the profits to be made by any strategy dry up pretty quickly as more shops discover it, so it does make sense to me that this doesn't appear to be done any more. I mean, isn't that what worked a few months ago doesn't work any more is the only thing most people posting about HFT can agree about? :D

I have no experience in electronic trading and my knowledge of it mostly comes from HN posts and - as you guessed correctly - Flash Boys, so please forgive my ignorance

> As I understand some order types were more or less designed to give HFT an edge.

And some order types are more or less designed to give large block traders an edge.

Most of the latency game you read about is not getting to trade, its getting the opportunity to cancel your orders. A common misconception is that HFT groups are acting as middle men. They aren't. They are the counter parties on all the exchanges, they are just updating what they are offering faster than others.

Sure. But, after interviewing a bunch of HFT developers over the last 6 months (because: reasons), the understanding I've developed is that "latency arbitrage" --- which is what you seem to be describing --- is no longer particularly profitable, or the focus of what most "HFT firms" do. Is my understanding broken?

No, the market evolved as it always does. But, so much of the "HFT is evil" belief stemmed from the subprime era and with respect to fair play at the time, you can't ignore the impact of NMS. I went back to grad school in 2010 and had to be careful to whom I told my background, else I'd get roped into some morality debate with a 26 year old Occupy activist who didn't know what a market order was.

Nowadays, I really don't see much edge in trading at all.

I would love to know what those traders you've spoken with think is profitable. I see my old bosses at Rom near the CME almost every Friday and I haven't heard a positive line from them in 5+ years.

Latency arbitrage is pretty much impossible as a newcomer and many firms are getting squeezed out of that particular opportunity. Think Jump, KCG, and Citadel...Jump/KCG both share satellites across the US...read more about the radio dish networks here: https://sniperinmahwah.wordpress.com/2014/09/22/hft-in-my-ba...

Simple latency arb strategies are totally an arms race now, with very high barriers to entry. That does not mean however that latency becomes unimportant - if you are a market maker you're essentially playing the same game in reverse - you want to move your quotes out of the way to avoid getting your lunch eaten by those aggressors.

I would argue that the HFT that gets all the negative press are those systems taking advantage of Reg NMS. I think the regulations that caused it should be removed. If you're looking for a black & white definition to satisfy the age old quest to define high frequency trading, you could pick worse.

There are other strategies that get a lot of bad press, of course, but they are not novel with respect to strategy, only speed. Deception is par for the course. And sometimes, products are just poorly designed. Leveraged ETFs, for example.

He could be saying but if so its not true. RegNMS trading is a thing. Latency arbitrage is also a thing. There are also a wide variety of strategies that may exploit the idiosyncrasies of a specific exchange. Multiple venues, while useful and common, are not needed in all HFT strategies.

My understanding is the reason you advocate for long gamma vs. short gamma because unhedged short gamma trade (e.g., short straddle) could cause theoretical unlimited loss. Long gamma trades like long straddle or long option hedged with delta-neutral stock, you are facing daily theta decay and you are betting for either a rise in implied vol or realized vol.

However, the missing ingredient/secret sauce is (1) you have to figure out at price point you're going to take profit in your scalp; and (2) when implied volatility is considered cheap for the particular ticker you're trading. Much appreciated for your insight and let me know if I'm missing anything.

You've got some model of richness/cheapness. From that, you have your raison d'etre and, when combined with your view on utility and expectations, a money management strategy. Putting all that together is your business.

My only opinion on the matter is that you should try to stick with leading from long gamma. You can sell vol, but you'll survive longer if you keep net long gamma. As soon as you get gamma'd, you're out of business. It can go so far against you before you even realize what happened.

There's a fairly big question of what human capital comes along with this. You will need some guys who are good at low latency programming.

Some strategies that I've seen also depend on having good agreements with brokers, ie you may see an opportunity in the data, but the costs of trading tip you into the red if your guy is margining you in a different way. I don't know what Lime et al charge you, but they aren't a likely name among the people I know.

There's also a question about what exactly you'll be doing in those markets. There are guys who make money market making options over the phone, without relying on colo for anything. Sometimes they'll have a quote machine that needs to be quick to pull, but they don't see it as anything other than a bit of extra money. Other options guys are totally different, relying entirely on speed to make their dough.

Also keep in mind you are only competing with HFT in as far as what you're doing is similar, ie there's a high chance you'll both want to grab the same trade.

I would say that even options/futures/and other products markets are just as hard to market make compared to the equities markets. In my opinion, you need some sort of edge not through hardware but through your model or your market outlook, combined with market-making/hft/statistical-arbitrage in order to be profitable and compete.

1) Capital in the magnitude of >$500k seems reasonable for a small operation

2) Lime Brokerage (a friend has started a hft strategy with a professor on campus and has tested out lime) is okay, I'd look into some other execution services as well

3) Yes you should be backtesting on tick-level data from multiple exchanges ideally. Be wary of lookahead bias and try to build some sort of execution model to account for how your executions might actually be filled and how your orders might affect the market microstructure

Ultimately, I wouldn't rely on pure hft and latency sensitive strategies...latency is always important but you should try to find your edge elsewhere.

This is something that comes to my mind every time there is a press release talking about HFT and the milliseconds advantage they use to make a profit.

I would love some comments from a seasoned HFT (tech) guy.

There exist in the trading space entities that look essentially like what the OP is suggesting. They are called prop trading firms, or quantitative trading firms, etc.

There are even entities that act like incubators for those entities.

Take what Jonathan Kinlay says about HFT with a grain of salt. He worked at a friend's firm briefly before leaving without making a single profitable strategy (although his excel models were profitable of course). While what he says in this article is in the ballpark of correct, he is not the best source of information on modern HFT.

I'm actually serious about this -- read anything on HFT strategies online with a grain of salt, because you are the type of person HFT firms are looking to exploit. In HFT it can be very hard to know if you're the hunter or the prey.

Some strategies that involve complex positions might post small daily returns. Then, an event can come along and wipe out a month of profit, or more. It's a shark eat shark world.

Right. HFT relies on finding arbitrage opportunities, which are limited and temporary. Unless you're building AI that will adjust to other players' strategies in real-time, you're behind the game.

It is nice to realise that people who clearly have stellar resumes still get this kind of knocking when sticking their heads above the parapet - it makes me feel worrying about the stuff people could say about me should not stop me from putting my head up more often.

Take what this commenter says about OP with a grain of salt. He had a friend that hired OP and seems to be bitter that OP left before he could profit off of him. While what he says may be in the ballpark of correct, an anon poster making ad hominem comments is not the best source of information on the OP.

One question I have is, when do you know to abandon a trading strategy that used to be profitable, but has not been profitable over the past N number of days. At what point do you throw in the towel and move onto another strategy?

You have to find out why it stopped working. Was it an aggressive strategy that used to have a 100% fill rate, but now is only getting filled on 30% of the orders it sends out? Chances are that you've just become too slow for that trade. The only fills you are getting now are the bad ones. Time to move on or speed up.

Let's say the fill % stays the same though. Has volatility in your market dropped off a cliff the past few weeks? Perhaps your strategy is highly dependent on volatility. It'd be good to keep this one running, as it's likely volatility will return at some point. You want to diversify though and have other strategies that perform well in such a low vol regime, so you're not dependent on high vol.

This would be an "aggressive" strategy. You get a signal from some source (looks like the author worked in news events, but the signal could be anything). If the signal indicates, via your model, that the product you are trading will go up through the best offer, you send an aggressive buy into that offer.

If all works out well, you get filled for a buy and the old offer (which you bought at) is now at least the best bid. Do this hundreds of times a day and you're starting to talk about real money, especially since you can scale (to a point) by upping your quantity.

Sometimes you aren't fast enough though. That buy you sent into the best offer is too slow - it merely appears as a buy at what is now the best bid (or doesn't at all if you use an IOC - immediate or cancel), and you get no trade. Even if you only get filled on 20% of the signals, if they are on average good, then you still make money.

This is just one type of strategy though. Not all HFT strategies rely on aggressive signals, though a lot do.

Just making a guess here but it may be that you have several limit orders fail to be filled for any given trade but when you you place an order that finally does get filled it may still complete a winning trade despite being your 5th order placed for the trade.

I tried this with bitcoins and that didn't work out so well. All your math formulas can be pointing up, but you never know what the human element will do...

Depends on what your definition of HFT is. But for every definition of it, deep pockets are relative & HFT is not any more capital intensive than lots of other industries & much less than most.

That is a very high bar to get over for any industry. For instance you could say the exact same thing about the internet generally and not come up with too many answers.

Another way to reason about it is A) how does HFT compare to the system it replaced? and B) what would we need to give up to not have HFT (if we decided for some reason we didn't want HFT, though I'd love to hear someone enumerate why we wouldn't want it).

A is trivial to answer. It is much, much cheaper for nearly everyone to trade with HFT than it was in the world of specialist market makers or pit traders. In the modern world there are much less middle men for every trade and they take a dramatically lower percentage of the value than the system they replaced. This is the obvious and expected outcome of replacing expensive humans with cheap computers.

B is also pretty trivial to answer. We would have to go to a monopoly exchange with no electronic communications into or out of it. I hope the downsides of that are obvious.

HFT replaces "expensive humans" with specialist computers that try to site right next to the trading servers, so they can take advantage of the speed of light.

So may I suggest a simpler alternative: Run a trading system with three chunks of time: "get orders", "serve orders", "rest". These intervals could he an hour or 15 seconds. But these way a phone on the otherside of the planet could put in a trade along with the speed of light computers, and not be at a disadvantage.

All HFT is doing is licking the cream off the top of the market -- and not providing any value that a more fair computerized trading system would provide.

Everyone will wait until just before the closing of the window, before submitting their orders, so that they trade with the most information available.

Those with fast connections will have more market information at the point that they place their order.

e.g. I phone in an order to buy gold at $1,200 one minute before the window close. The gold price rises to $1,300. A fast-connection trader then offers $1,201 and buys all the cheap gold, leaving my order unfilled.

Your simpler alternative is known as a batch auction. It exists already in the electronic trading space and typically they have the reputation for being more gamed, not less that traditional order book exchanges.

There was a pretty popular paper out of U of Chicago that showed that a monopoly exchange using batch auctions was "better" for most market participants. That paper did not take into account a few major points that seem (at least to me) relevant.

- The monopoly auction would need to be across all exchanges globally to prevent venue arbitrage. That is not only would you need to unify all of the US equity markets with all of the US futures/options/derivatives markets you would need to do that globally. No German commodities, no Japanese equities, etc. That seems...unlikely. Without a unified monopoly exchange there still exists a speed advantage for colocation.

- The paper did not include execution costs, either in the form of technology drag or fees. On a monopoly exchange that seems important.

Finally, when thinking about batch auctions (or any exchange algorithm for that matter) you need to account for tie breakers. That is, assuming you are still doing price priority (highest buy price wins, lowest sell price wins) then what happens when at the end of your auction there are more buyers or sellers at a given price than can be filled? Some options:

- price/time - this is the traditional matching rules. The order that has been in the order book longest wins. It obviously creates races.

- pro rata - this is another form of matching that currently exists that gives precedence to larger orders, generally by filling a percentage of your order based on the percentage of the total orders at a price it represents. This does not have as many race conditions (though cancel speeds continue to be super important in these markets, maybe less so in a batch auction version). But it gives significant advantages to big market participants or those who are willing to game their risk metrics. In those marketplaces the liquidity is dramatically over reported (a common complaint of HFT) and small order market participants typically must pay the bid/ask spread to get filled. In effect, you can't trade unless you are willing to pay the big boys in these markets.

- random - this is a common idea, and is theoretically more fair (in the mathematical sense) but think about what it would mean. If you put an order in 6 months ago and watched as the price worked its way towards your position, you would have no better chance of getting filled at that order price than someone who just added an order at the last second. This in fact encourages races, not discourages them! Further, it is trivially gamed. It would provide incentives for market participants to flood the auction with small 1 lot orders, again inflating "real" liquidity, in order to increase their chances of getting filled.

All of these still have advantages for participants who are faster, especially on the cancel side. I believe it is a fundamental part of the markets, that spending more resources on monitoring them provides an advantage. There may be other matching algorithms, but these are the ones commonly proposed.

There is a much simpler way to make latency less important than to go to batch auctions or monopoly exchanges. It is to allow for massive decimal places in pricing. That is instead of going down to the penny, go down to the 1/10000 of a penny. That doesn't allow humans any advantage, but it makes the machines compete on what we want them to compete on, price. Note, that full time computerized trading in this format is still at an advantage to phone based humans.

As an aside, a couple of specific points to your comment:

> HFT replaces "expensive humans" with specialist computers that try to site right next to the trading servers

Those computers are dramatically cheaper than the humans they replaced, who were also colocated with the exchange at much higher prices. The savings are passed onto you the consumer as HFT is an extremely low margin business at this point.

> All HFT is doing is licking the cream off the top of the market

This makes me think you have a incorrect (though common) view of how HFT works. You seem to be of the opinion that HFT is stepping into trades that would already happen, ie you are going to trade with another party and the HFT uses their nefarious speed to take money from the both of you. That is not so. The other party is the HFT. Don't think of them as scalping your trade, think of them as adjusting their own prices.

Rather than subverting the price discovery mechanism the market is so famous for, HFT is the price discovery mechanism and it is a far more efficient one than any of the other options we've come up with yet.

{kind=link}

I imagine HFT entities who are broker-dealer agencies have even lowered fee structure; but it sounds like simple market-making on equities is no longer an easy business to be in due to the lowered spreads and crowded competitors.

So I'm wondering if a startup funds with the rented access could compete with the big boys in the options, futures, other derivatives and even bonds space where the latency still haven't caught with the equity market yet.